Blockchain is a new technology, which is known as Distributed Ledger Technology (DLT). With the help of Blockchain technology, currency as well as anything can be converted into digital format and stored.

Blockchain was first proposed in 1991 as a research project, but in the year 2009, Blockchain was used in bitcoin. Bitcoin is a cryptocurrency which is built on the basis of Block technology.

Blockchain has since been used in the creation of various cryptocurrencies, decentralized finance applications, non-fungible tokens and smart contracts.

Must read: Blockchain Technology

What is a Blockchain?

Blockchain is a shared immutable ledger that facilitates the process of recording transactions and tracking assets across a business network. Anything of value can be tracked and traded on the Blockchain network.

A Blockchain is a distributed database, which is shared over a computer network.

Blockchain stores information electronically in a digital format to make transactions secure.

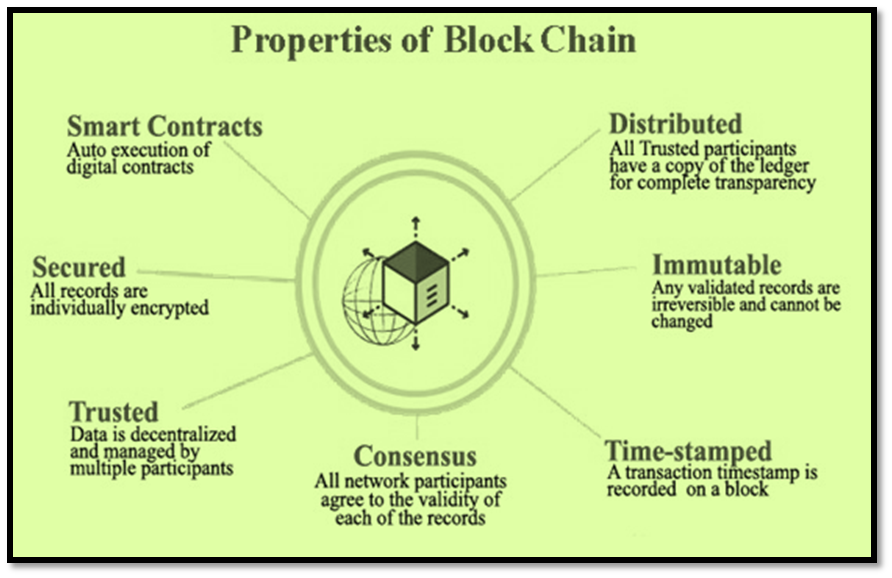

Properties and elements of a blockchain

Distributed ledger technology

All network participants have access to the distributed ledger and its immutable record of transactions. With this shared ledger, transactions are recorded only once, eliminating the duplication of effort that’s typical of traditional business networks.

Immutable records

No participant can change or tamper with a transaction after it’s been recorded to the shared ledger. If a transaction record includes an error, a new transaction must be added to reverse the error, and both transactions are then visible.

Smart contracts

To speed transactions, a set of rules that are called a smart contract is stored on the blockchain and run automatically. A smart contract defines conditions for corporate bond transfers, include terms for travel insurance to be paid and much more.

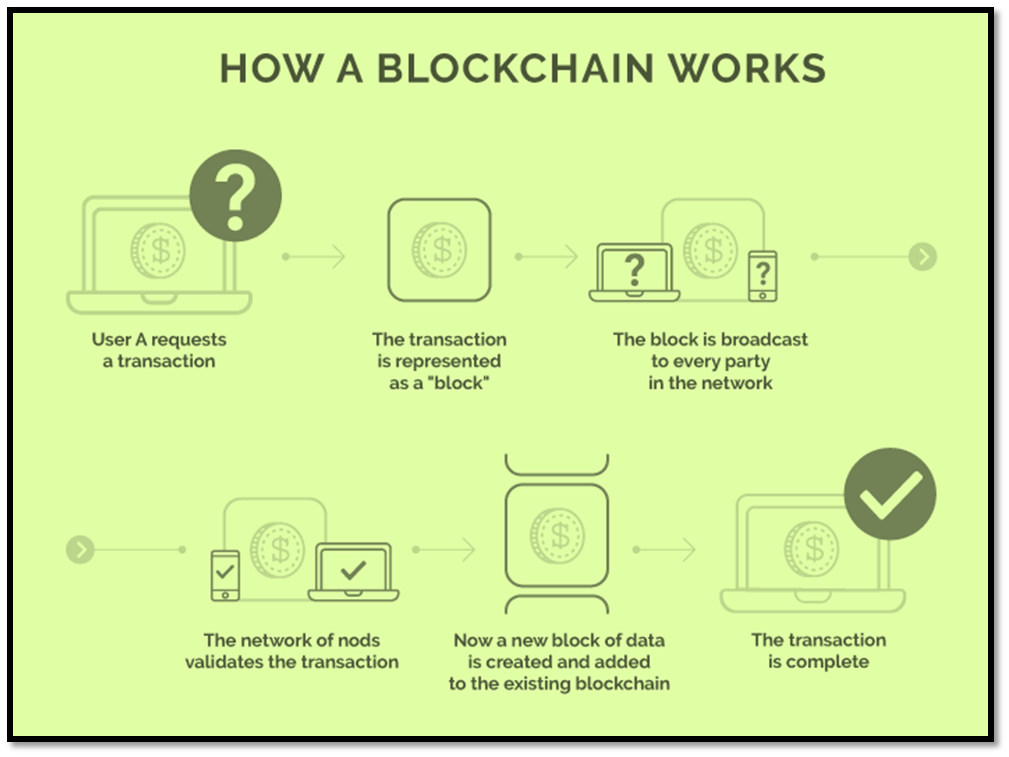

How blockchain works?

As each transaction occurs, it is recorded as a “block” of data. Those transactions show the movement of an asset that can be tangible (a product) or intangible (intellectual).

The data block can record the information of your choice: who, what, when, where, how much. It can even record the condition, such as the temperature of a food shipment.

Each block is connected to the ones before and after it. These blocks form a chain of data as an asset moves from place to place or ownership changes hands.

The blocks confirm the exact time and sequence of transactions, and the blocks link securely together to prevent any block from being altered or a block being inserted between two existing blocks.

Transactions are blocked together in an irreversible chain: a blockchain.

Each additional block strengthens the verification of the previous block and hence the entire blockchain. Rendering the blockchain tamper-evident, delivering the key strength of immutability.

Uses of Blockchain

Banking and Finance

By integrating blockchain into banks, consumers might see their transactions processed in minutes or seconds—the time it takes to add a block to the blockchain, regardless of holidays or the time of day or week. With blockchain, banks also have the opportunity to exchange funds between institutions more quickly and securely.

Blockchain could drastically reduce the time in settlement and clearing process for stock traders.

Currency

Blockchain forms the bedrock for cryptocurrencies like Bitcoin. Blockchain can give those in countries with unstable currencies or financial infrastructures a more stable currency and financial system. They would have access to more applications and a wider network of individuals and institutions with whom they can do domestic and international business.

Healthcare

Healthcare providers can leverage blockchain to store their patients’ medical records securely. These personal health records could be encoded and stored on the blockchain with a private key so that they are only accessible to specific individuals, thereby ensuring privacy.

Property Records

Blockchain has the potential to eliminate the need for scanning documents and tracking down physical files in a local recording office. If property ownership is stored and verified on the blockchain, owners can trust that their deed is accurate and permanently recorded.

Smart Contracts

A smart contract is a computer code that can be built into the blockchain to facilitate a contract agreement. Smart contracts operate under a set of conditions to which users agree. When those conditions are met, the terms of the agreement are automatically carried out.

Supply Chains

Suppliers can use blockchain to record the origins of materials that they have purchased. This would allow companies to verify the authenticity of not only their products but also common labels such as “Organic,” “Local,” and “Fair Trade.” The food industry is increasingly adopting the use of blockchain to track the path and safety of food throughout the farm-to-user journey.

Voting

Blockchain could facilitate a modern voting system. Voting with blockchain carries the potential to eliminate election fraud and boost voter turnout. The blockchain protocol would also maintain transparency in the electoral process, reducing the personnel needed to conduct an election and providing officials with nearly instant results.

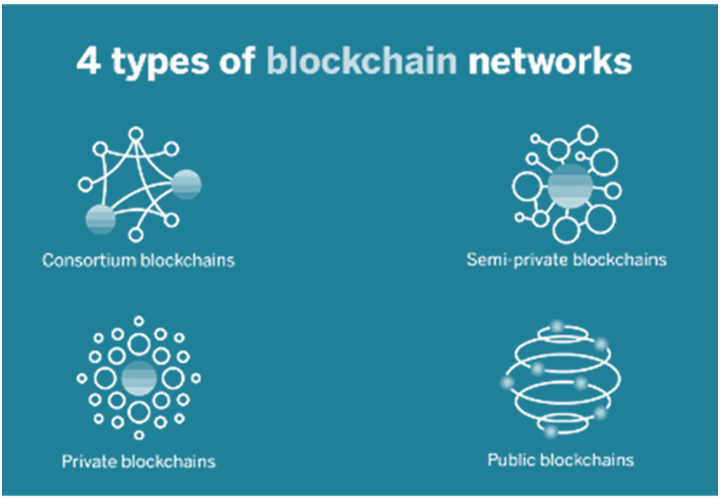

Types of blockchain networks

There are several ways to build a blockchain network. They can be public, private, permissioned, or built by a consortium.

Public blockchain networks

A public blockchain is one that anyone can join and participate in, such as Bitcoin. Drawbacks might include the substantial computational power that is required, little or no privacy for transactions, and weak security. These are important considerations for enterprise use cases of blockchain.

Private blockchain networks

A private blockchain network, similar to a public blockchain network, is a decentralized peer-to-peer network. However, one organization governs the network, controlling who is allowed to participate, run a consensus protocol and maintain the shared ledger. Depending on the use case, this can significantly boost trust and confidence between participants. A private blockchain can be run behind a corporate firewall and even be hosted on premises.

Permissioned blockchain networks

Businesses who set up a private blockchain will generally set up a permissioned blockchain network. It is important to note that public blockchain networks can also be permissioned. This places restrictions on who is allowed to participate in the network and in what transactions. Participants need to obtain an invitation or permission to join.

Consortium blockchains

Multiple organizations can share the responsibilities of maintaining a blockchain. These preselected organizations determine who submit transactions or access the data. A consortium blockchain is ideal for business when all participants need to be permissioned and have a shared responsibility for the blockchain.

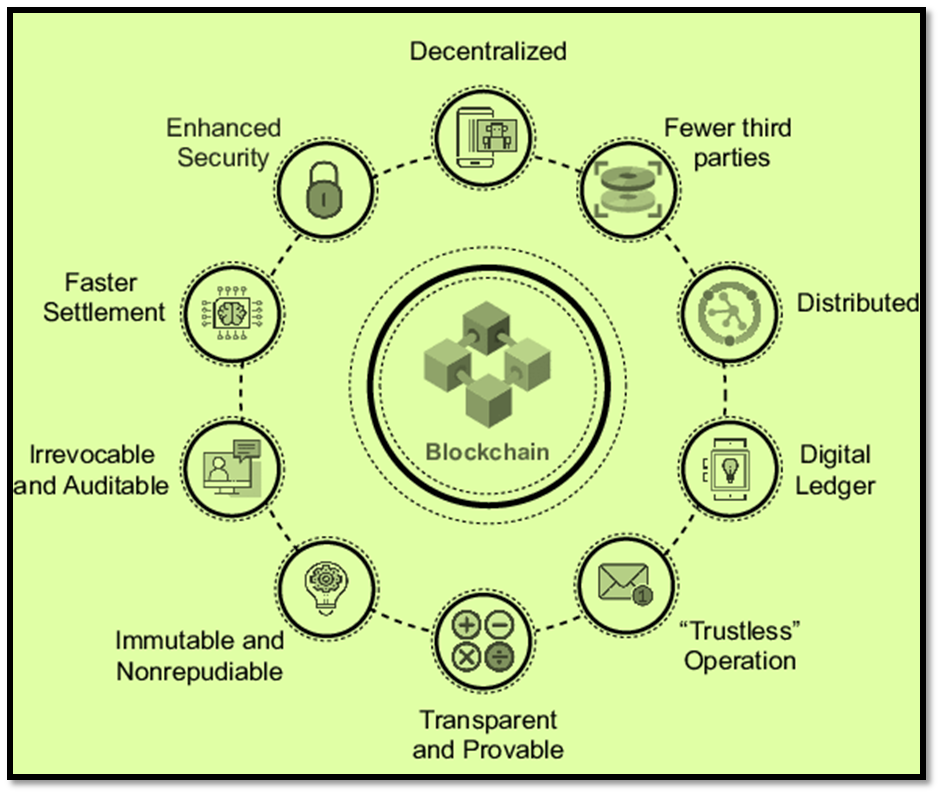

Benefits of Blockchains

Greater trust

With blockchain, as a member of a members-only network, you can rest assured that you are receiving accurate and timely data. And that your confidential blockchain records are shared only with network members to whom you granted access.

Accuracy of the Chain

Transactions on the blockchain network are approved by thousands of computers and devices. This removes almost all people from the verification process, resulting in less human error and an accurate record of information.

Greater security

Consensus on data accuracy is required from all network members, and all validated transactions are immutable because they are recorded permanently. No one, not even a system administrator, can delete a transaction. The blocks cannot be altered once the network confirms them.

Cost Reductions

Typically, consumers pay a bank to verify a transaction or a notary to sign a document. Blockchain eliminates the need for third-party verification—and, with it, their associated costs.

Decentralization

Blockchain does not store any of its information in a central location. Instead, the blockchain is copied and spread across a network of computers. Whenever a new block is added to the blockchain, every computer on the network updates its blockchain to reflect the change. By spreading that information across a network, rather than storing it in one central database, blockchain becomes more difficult to tamper with.

More efficiencies

Transactions placed through a central authority (Financial institutions) can take up to a few days to settle. But a blockchain works 24 hours a day, seven days a week, and 365 days a year. On some blockchains, transactions can be completed in minutes. With a distributed ledger that is shared among members of a network, time-wasting record reconciliations are eliminated.

Private Transactions

Many blockchain networks operate as public databases, meaning anyone with an internet connection can view a list of the network’s transaction history. Although users can access transaction details, they cannot access identifying information about the users making those transactions.

Transparency

Most blockchains are entirely open-source software. This means that everyone can view its code. This gives auditors the ability to review cryptocurrencies like Bitcoin for security.

Banking the Unbanked

Perhaps the most profound facet of blockchain and cryptocurrency is the ability for anyone, regardless of ethnicity, gender, location, or cultural background to use it. According to The World Bank, an estimated 1.3 billion adults do not have bank accounts or any means of storing their money or wealth.

These people are often paid in physical cash. They then need to store this physical cash in hidden locations in their homes or other places, incentivizing robbers or violence. While not impossible to steal, crypto makes it more difficult for would-be thieves.

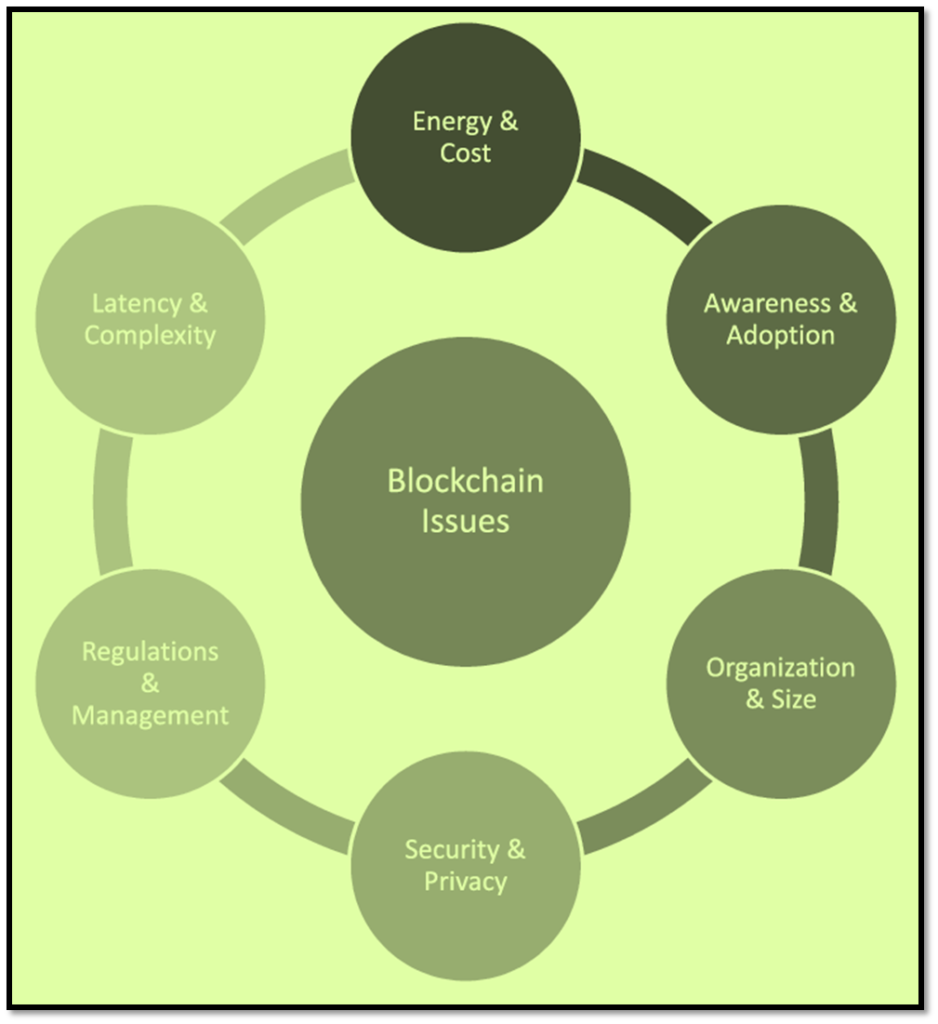

Limitations of Blockchains

Technology Cost

Although blockchain can save users money on transaction fees, the technology is far from free. For example, the Bitcoin network’s proof-of-work system to validate transactions consumes vast amounts of computational power.

Speed and Data Inefficiency

Bitcoin is a perfect case study for the possible inefficiencies of blockchain. Bitcoin’s PoW system takes about 10 minutes to add a new block to the blockchain. At that rate, it’s estimated that the blockchain network can only manage about three transactions per second (TPS).

The other issue is that each block can only hold so much data. The block size debate has been and continues to be one of the most pressing issues for the scalability of blockchains going forward.

Illegal Activity

While confidentiality on the blockchain network protects users from hacks and preserves privacy, it also allows for illegal trading and activity on the blockchain network.

The dark web allows users to buy and sell illegal goods without being tracked by using the Tor Browser and make illicit purchases in Bitcoin or other cryptocurrencies.

Regulation

Many in the crypto space have expressed concerns about government regulation over cryptocurrencies. While it is getting increasingly difficult and near impossible to end something like Bitcoin as its decentralized network grows, governments could theoretically make it illegal to own cryptocurrencies or participate in their networks.

Conclusion

Business runs on information. The faster information is received and the more accurate it is, the better. Blockchain is ideal for delivering that information because it provides immediate, shared, and observable information that is stored on an immutable ledger that only permissioned network members can access.

A blockchain network can track orders, payments, accounts, production and much more. And because members share a single view of the truth, you can see all details of a transaction end to end, giving you greater confidence, and new efficiencies and opportunities.

External link: https://en.wikipedia.org/wiki/Blockchain